Vanguard Australia recently announced their newly launched Vanguard Personal Investor product in Australia. Which is actually a Vanguard created ASX stock brokerage account with $0 brokerage on all Vanguard ETFs and managed funds. That’s right $0 brokerage on the ASX, but there are definitely some catches which you need to be aware of.

Update: Vanguard Australia updated their fee structure on the 18th August 2021. I’ve done an updated review going over this new structure here.

So in this post I’m going to share with you guys a detailed review of the Vanguard Personal Investor offering in Australia, and how it stacks up compared to purchasing Vanguard ETFs through another stock broker, and also how it compares to buying directly through Vanguard Retail or Wholesale Funds. This way you will know in exactly which situations it will be optimal for you to be using the Vanguard Personal Investor in Australia, as it is not that straightforward.

What/who is Vanguard?

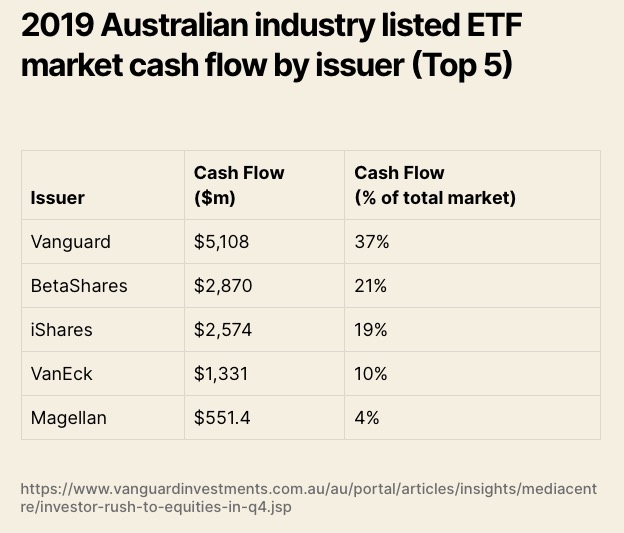

For those of you who don’t know who or what Vanguard is, I’ll keep this brief but Vanguard is a fund manager and is actually the largest provider of mutual funds in the world. And in Australia, they are by far the most popular fund manager and ETF manager in the country. 2019 was a record year for Vanguard ETFs, with Vanguard ETF Assets Under Management (AUM) growing to $19.5B, making 2019 Vanguard’s strongest year since launching their first ETF on the ASX 10 years ago.

Vanguard Personal Investor Australia Overview

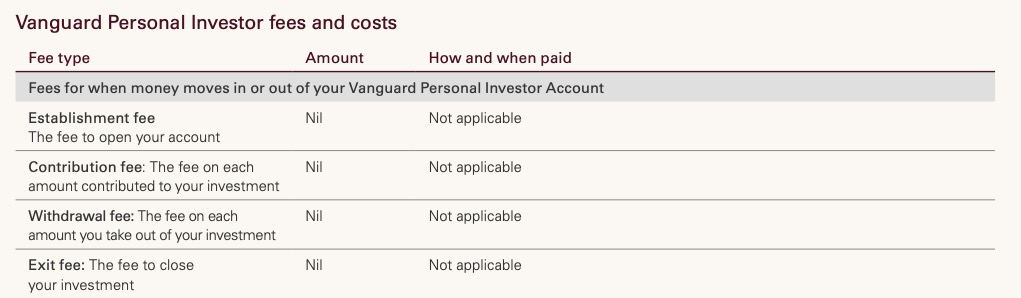

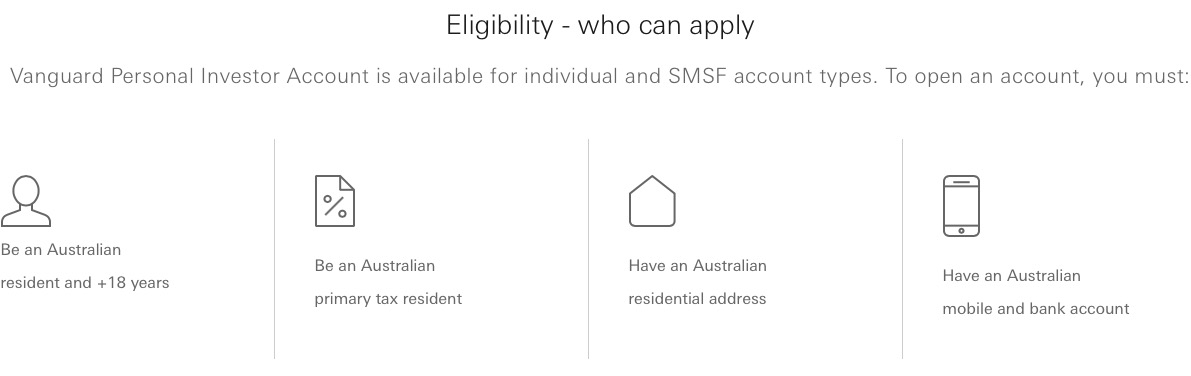

However today we’re going to look into Vanguard’s newest product which is the Vanguard Personal Investor. So in terms of who can use it, basically you just need to be an Australian resident and over 18, nothing too complicated here. And in terms of fees for setting up the account there’s nothing here. With no fees for opening up an account, no fees for transferring funds into the account and no withdrawal or exit fees. Which is great.

Vanguard Personal Investor Features

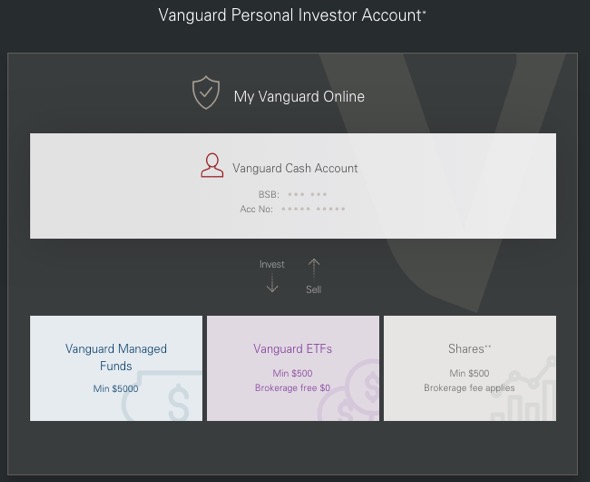

In terms of the feature set you get when signing up to the Vanguard Personal Investor. There are 4 main elements of the product which I’ll break down. They have the Vanguard Cash Account, Vanguard ETFs, Vanguard Managed Funds, and the rest of the ASX.

Vanguard Cash Account

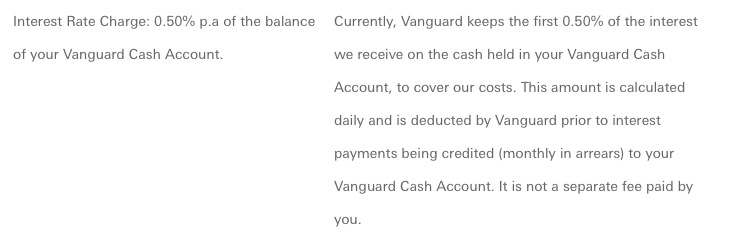

You get a Vanguard Cash Account which is essentially like a regular cash account that you have with any stock broker, except unlike a lot of the other competitors in Australia, the vanguard cash account actually receives an interest return, which is currently 0.50% p.a which sounds decent on paper. However this is a little bit deceptive, as I will show you.

Firstly, it was extremely difficult to actually find what the current interest rate was. If you start on the main page it tells you nothing about the interest rate, however if you scroll right to the bottom you can find the Vanguard Personal Investor Part B – Statement of Additional Information. Which does make reference to the interest on your Vanguard Cash Account, however it doesn’t actually tell you the rate and again points you to another link. However clicking this link just takes you to the main Vanguard Personal Investor page, with again, no reference to the interest rate on the cash account. I was finally able to find if you go to the Fees and costs page of the personal investor page, You are able to find a section talking about the “competitive interest rate” where they have a link to a PDF with the actual interest rate.

Don’t ask me why the only way to see the interest rate return is in the fees section of the website.

But I think I found why, I think it’s meant to act as a bit of distraction. Because if you scroll down to the bottom of the same page, you actually find that they again talk about the interest rate on the Vanguard Cash Account, and again being 0.50% p.a.

However this is where you need to be careful not to be confused, this is not referencing the 0.50% return you get on your money in the cash account. This is actually another fee that is charged by Vanguard. Basically on any interest you earn from funds in your cash account, Vanguard will take 0.5% of that. So say you had $1,000 in there, in a year you would earn a 0.5% return, which would be $5, however Vanguard will take 0.5% of that, which is only 2 and half cents, leaving you with $4 and 97 and a half cents? But it doesn’t stop there.

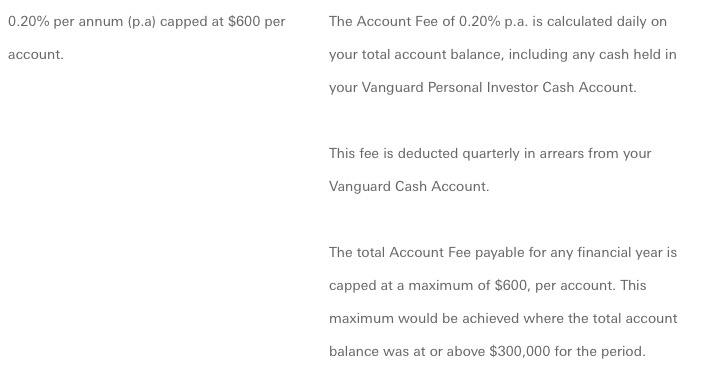

Vanguard actually charges an additional fee of 0.20% p.a on your whole account balance, including your cash account, which on $1,000 + your interest return of $4.975 after a year ends up being about $2 ($2.00995). Leaving you with just under $3 ($2.96505) in actual returns. So the actual interest rate you’re getting is not 0.50% p.a and is actually just under 0.3% p.a (0.296505%).

Granted this is still better than the 0% interest return offered by the majority of other ASX brokers but they lose points here for not being more transparent with the true return.

Investing in Vanguard ETFs using Vanguard Personal Investor Australia

Next let’s have a look at the actual investment options that you have within the Vanguard Personal Investor. With their headline feature being $0 brokerage fees on purchasing any Vanguard ETF listed on the ASX, which is honestly a pretty amazing feature with nothing close being offered by any other ASX broker in Australia. And there aren’t really any catches with this, you just need a minimum transaction size of $500 and you can purchase any Vanguard ETF investment for free. However there are a few things you do need to be aware of.

First, that 0.20% p.a fee I talked about earlier applies to your whole Vanguard Personal Investor account balance, so if you had $10,000 in Vanguard ETFs you would be charged $20 a year. And of course there isn’t any fee like this associated with other ASX brokers, so really you’re paying for “free brokerage” through this yearly fee. However if you find that your brokerage costs for buying Vanguard ETFs is more than the yearly fee, then you can come out ahead here. Also the fee is capped at $600 a year, so once your entire balance starts to grow over $300,000, this fee becomes much smaller as a percentage of your total balance and you’ll be able to come out ahead here as well.

The next thing you need to be aware of is that 0.20% p.a fee does not exclude you from the fees associated with each individual ETF itself. So this will be exactly the same as if you were purchasing Vanguard ETFs via any other broker. For example with VAS you’re still going to be charged 0.10% p.a for management fees of that ETF. But that’s it, and really this is where the Vanguard Personal Investor shines, and is a good option if you’re regularly only buying Vanguard ETFs. If you’re wondering which Vanguard ETFs would be good to pick up, check out my post on the Best Vanguard ETFs on the ASX. Later I’ll actually break this down in detail and show you guys the exact inflection points at which it’s better to use the Vanguard Personal Investor vs another ASX broker.

Investing in Vanguard Managed Funds using Vanguard Personal Investor Australia

But before that let’s look at the 2 other investment options within the product. First, Vanguard Managed Funds. One big bonus of using the Vanguard Personal Investor is that you get access to the wholesale managed funds which normally have a $500,000 minimum balance requirement, these have much lower fees than their retail managed funds.

However the wholesale funds have higher fees than their equivalent ETFs and there’s almost no situation in which I would recommend you use the managed funds over the ETFs. The only small benefit is that they have no minimum investment amount (other than the initial $5,000). So if you prefer investing in small parcels of less than $500 (the minimum transaction size for ETFs) then that is one small benefit for the managed funds. But in the long run it’s really not worth it. If we look at Vanguard Australian Shares for example , the ETF has a management fee of 0.10% p.a, whereas the equivalent wholesale managed fund has a fee of 0.16% p.a. And just to clarify you still need to pay the 0.20% p.a fee for any funds invested in the managed funds as well.

Investing in Non-Vanguard Stocks/ETFs using Vanguard Personal Investor Australia

The last investment option using the Vanguard Personal Investor is buying non-Vanguard shares or ETFs on the ASX. I’ll keep this one really brief, the personal investor is terrible for this. If you’re going to be investing in shares or ETFs on the ASX other than Vanguard ETFs do not use the Vanguard Personal Investor.

To start with they have brokerage fees of $19.95 or 0.15% of the value (whichever is greater). Compare this with SelfWealth (current cheapest in Australia) who have a fixed cost of $9.50 trade no matter the value. However remember you’re also being charged 0.20% p.a on your entire portfolio, this includes any non-Vanguard ETFs. Again, if you’re investing in shares or ETFs other than Vanguard ETFs do not use this product and instead use a low cost broker like Pearler (sign up with this link for 5 free trades). Full review on Pearler here.

Vanguard Personal Investor Australia Review Verdict

Now I know it sounds like I’ve been blasting the Vanguard Personal Investor, but the truth is it can be good depending on your circumstances which I’ll go into now.

For example let’s say you primarily invest in 2 Vanguard ETFs and the balance of these is $50,000 and you were purchasing additional units every month. With SelfWealth you would have paid $228 in brokerage fees in a year, which actually works out to be 0.456% p.a on a balance of $50,000. Compare this with Vanguard Personal Investor where you would have paid no brokerage fees but instead 0.20% p.a which comes out to $100 for the year. Which is less than if you were with SelfWealth.

So basically you just need to work out how much you estimate you would spend on brokerage fees on Vanguard ETFs in a year and if that works out to be more than 0.20% p.a of your total Vanguard ETF value then it makes sense to use the Vanguard Personal Investor for your Vanguard ETFs. And if the value of your Vanguard ETFs is greater than $300,000 than it definitely makes sense to use the product as you would be hitting the fee cap of $600 a year. Which is a little ironic since it’s marketed as a simple easy to use solution for new investors, when really the greatest benefit is for seasoned investors with large portfolio balances.

But overall I do think it’s a decent product and I’m glad they brought it to market. However I do think Vanguard could rethink some of the fees and at least make the non-Vanguard share purchasing a lot more cost-effective, if they really want to drive greater adoption of the product.

Personally I don’t use the Vanguard Personal Investor and don’t plan on using it currently. This is mainly because the ETF market in Australia has become extremely competitive and there are a lot of lower fee alternatives to many popular Vanguard ETFs, for example A200 (0.07% p.a) vs VAS (0.10% p.a) and DHHF (0.26% p.a) vs VDHG (0.27% p.a). I also mainly hold ETFs from funds other than Vanguard so it wouldn’t make sense for me personally.

So with that said you guys thank you so much for reading I really appreciate it. Let me know in the comments what other topics you would like me cover or if you have any questions.

https://www.google.com.sb/url?q=https://blender.community/lakeking/

https://uichin.net/ui/home.php?mod=space&uid=2661068

https://www.nlvbang.com/home.php?mod=space&uid=2978911

https://brycefoster.com/members/beerdock16/activity/1587081/

https://www.google.st/url?q=https://graph.org/Rejting-TOP-sajtov-astrologii-2026-onlajn-s-tochnymi-prognozami-04-28-3

https://bookmarking.stream/story.php?title=REITING-TOP-SAITOV-ASTROLOGII-2026-ONLAIN-S-TOCHNYMI-PROGNOZAMI-2#discuss

куспид овен телец мужчина читайте на омниватике (omnivatic.com) – полный астрологический прогноз для каждого

двойняшки гадание онлайн бесплатно пермский оракул гадать читайте на омниватике (omnivatic.com) – полный астрологический прогноз для каждого

что означают цифры на часах 22 33 читайте на омниватике (omnivatic.com) – полный астрологический прогноз для каждого

алексей и марина совместимость читайте на омниватике (omnivatic.com) – полный астрологический прогноз для каждого

5 аркан причина расставания читайте на омниватике (omnivatic.com) – полный астрологический прогноз для каждого

рассчитать лилит по дате рождения читайте на омниватике (omnivatic.com) – полный астрологический прогноз для каждого

новости спорта читали когда нибудь что то подобное?

https://omnivatic.com/category/lev/ читали когда нибудь что то подобное?

Лунный календарь читали когда нибудь что то подобное?

бкрадар читали когда нибудь что то подобное?

Расклад таро онлайн читали когда нибудь что то подобное?

расклад таро читали когда нибудь что то подобное?

casino south africa play game slot online casino in south africa

luminous south africa play game slot online casino in south africa

online casino south africa play game slot online casino in south africa

online casino south africa play game slot online casino in south africa

play game slot online casino in south africa

luminous casino south africa play game slot online casino in south africa

ставки на спорт – все спортивные события в одном месте на http://WWW.BKRADAR.COM

ставки на футбол – все спортивные события в одном месте на http://WWW.BKRADAR.COM