In this post we explore net worth across different age groups of Australian’s and how much you need to save in Australia at each age to be in line with the median.

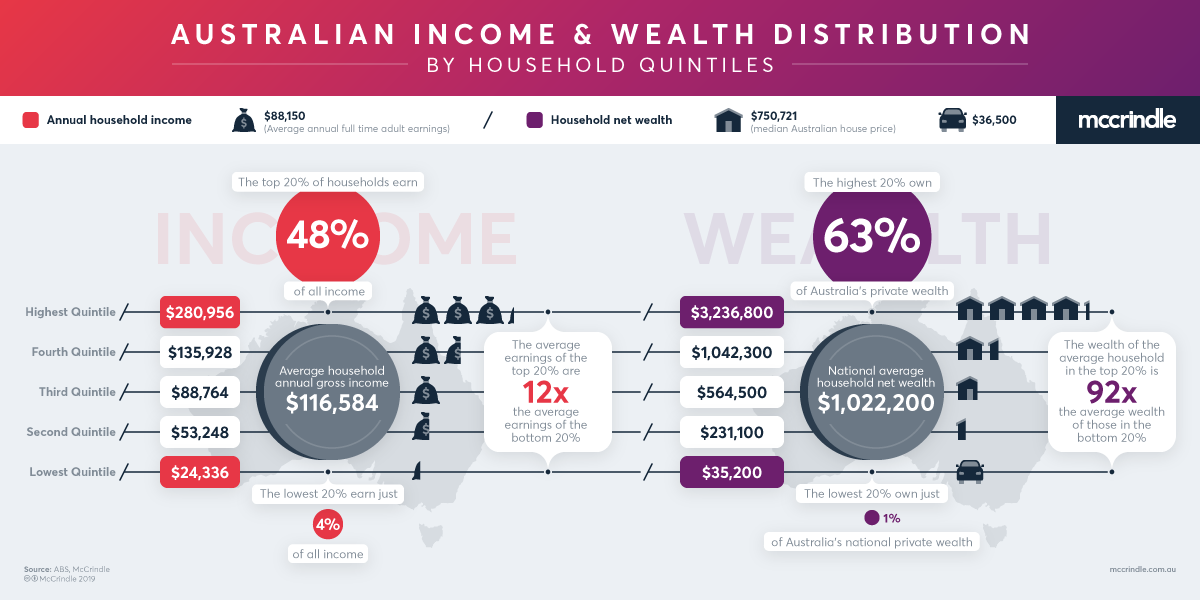

The wealthiest 20% of Australians have a 63% share of the total Australian wealth, with an average net worth of $3.2M. Compare this with the bottom 20% who have just a 1% share of total Australian wealth and an average net worth of just $35K. This means that someone in that top 20% in Australia has on average 92 times more wealth than someone in the bottom 20%.

What we’re going to do today is look into Australian net worth by age brackets, and see 1) what average looks like in Australia, 2) where you sit on the Australian net worth spectrum, and 3) what to do if you’re slightly behind. And whilst it’s never a good idea to compare with others when it comes to money, as everyone’s situation is unique, it does at least give us some benchmarks to think about or goals to strive for if we are aiming to become financially independent. And at the very least give you some specific actions to take if you do find that you are slightly behind your own personal financial goals.

As the important thing to note here is that whether you’re fresh out of school, well into your career, or forging your path through life, it’s never too late to start saving or to check to see that you’re heading in the right direction.

How to calculate your net worth

Calculating Net Worth

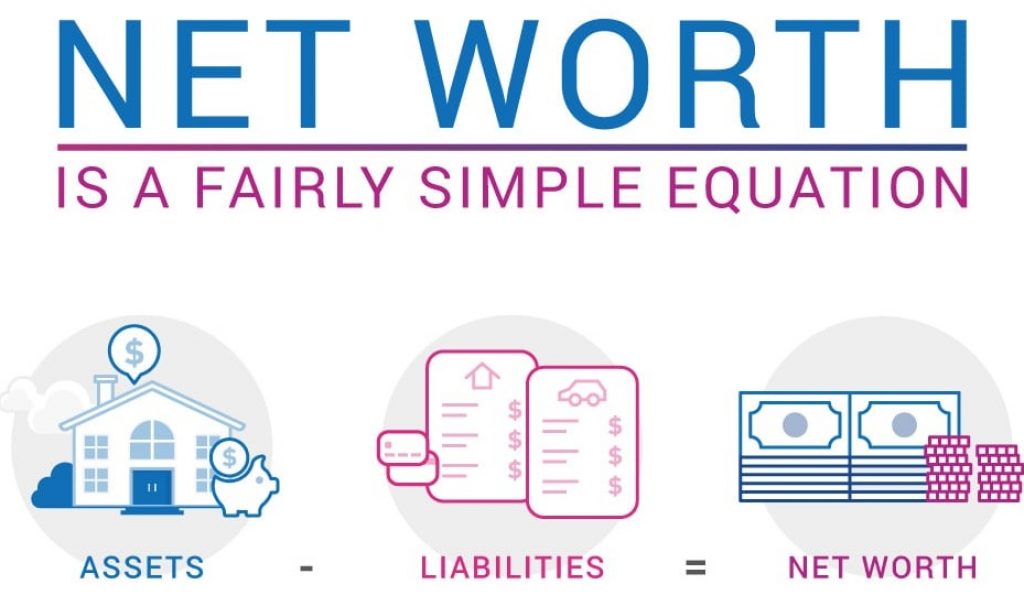

Now calculating your net worth isn’t really difficult. It’s much easier than you think. All you need to do is tally up everything you own of value to calculate your total assets, these will be things like:

- Non-financial assets, such as homes and their contents, land, and vehicles

- The value of any businesses you might personally own

- Other financial assets such as savings, shares, superannuation accounts

And then add up the value of any outstanding debts or loans to calculate your total liabilities, which may include:

- Mortgages

- Investment loans

- Credit card debt

- Borrowings from other households

- Other personal and study loans

Then all you need to do is subtract the total value of all your liabilities from your total assets. The total value is what is considered to be your personal net worth. Your total could result in a positive net worth or a negative net worth. If you’re in the negative net worth category, don’t stress too much, it’s alright. It’s typical for people who are early in their careers to have a low or negative net worth if they have student loans, or are new homeowners, or are just starting to save for the future.

20 years old

Average (Median) Net Worth At 20 Years Old: -$2,430

Which is a nice little segway to our first age bracket at 20 years old. If you’re 20 years old in Australia and have a $0 net worth, congratulations you’re doing better than most. I am not kidding, it’s pretty normal not to have any savings at this point of your life. Let’s face it. If you are in university and you’ve paid for it using HECS (or I think it’s called HELP now), even if you’re working part-time, it’s unlikely to be enough to pay off your entire university costs and living expenses.

Hence why the median net worth of a 20 year old in Australia is -$2,430, and note I am using median here not the mean, which is the value of someone in the 50th percentile. Median is a much better representation of average net worth, as the mean is completely blown out by the top percentiles who have super high net worths which drag up the mean.

However this doesn’t mean you can sit back and be okay with being in debt at 20, and we want to be better than average as it’s actually the best time in your life to start building good financial habits that will allow you to be ahead of the pack. So my challenge to you is if you’re in your 20’s make sure you have ticked off or are in the process of ticking off the following things.

Reduce expenses as much as possible. This doesn’t mean eating instant noodles every meal, but it does mean saving where possible when you do buy things. For example make sure you are always using a cashback site like Cashrewards or Shopback when shopping online, and you’re always shopping around for the best price. It’s okay to buy things you need but it’s definitely not okay to unnecessarily pay 20% more because you were too lazy to do a quick google search.

Avoid getting into any bad debt. When I say bad debt here, I mean debt for anything that isn’t providing you with a positive ROI, so this excludes things like your student loans and home loans. But basically most other forms of debt you want to avoid at this point, like personal loans, car loans and credit card debt.

Next if you weren’t able to avoid getting some bad debt, pay it down asap. Here’s my reasoning with this one, when you invest your money in a broad index fund or in real estate, or most investments for that matter on average you would expect anywhere between a 6-12% return on your money. And to get that type of return you’re gonna be risking some years in which you will actually end up losing money. On the other hand when you have high interest rate debt just paying down that debt is like getting a guaranteed instantaneous return on your money at whatever rate the interest rate of the debt is. So going and paying off a 20% interest rate on a credit card balance is almost like you getting an immediate guaranteed 20% return on your money with no risk whatsoever. So my basic rule of thumb is if you’re paying above 5% interest rates then it’s probably best you just throw as much money at that debt to pay it down as possible because you’re getting a similar return as to what a good investment would generate after paying taxes on it anyway.

Now if you’re 20 and aren’t in any debt the #1 thing to do is set up an emergency fund, which is just some money you set aside to only be used in case of (you guessed it) an emergency. This is usually around 3-6 months worth of living expenses and I recommend keeping it in a separate high-interest rate savings account.

Now lastly if you’ve already done all those things, this is now a great time to get started with learning how to invest and begin investing small amounts. I’d recommend checking out both micro-investing apps and passive ETFs to begin with. If you’re interested in learning more about investing with ETFs, check out my ETF beginners guide which will provide a solid outline of how to get started.

30 years old

Average (Median) Net Worth At 30 Years Old: $31,025

This brings us to the next milestone which is 30 and it’s insane to see how much lower the median value is compared to the mean value. Because the mean net worth for 30 year olds in Australia is actually $79,200 and that number is so skewed by the people in the top tenth percentile that it really isn’t a good representation of what the average 30 year old is worth. The median however is, and the median net worth for 30 year olds is actually $31,025, which is roughly half the average salary in Australia. Most money guides suggest that you should try and target to have a net worth at 30 equivalent to 1 year of your salary, which to be honest seems like a fairly reasonable goal to target.

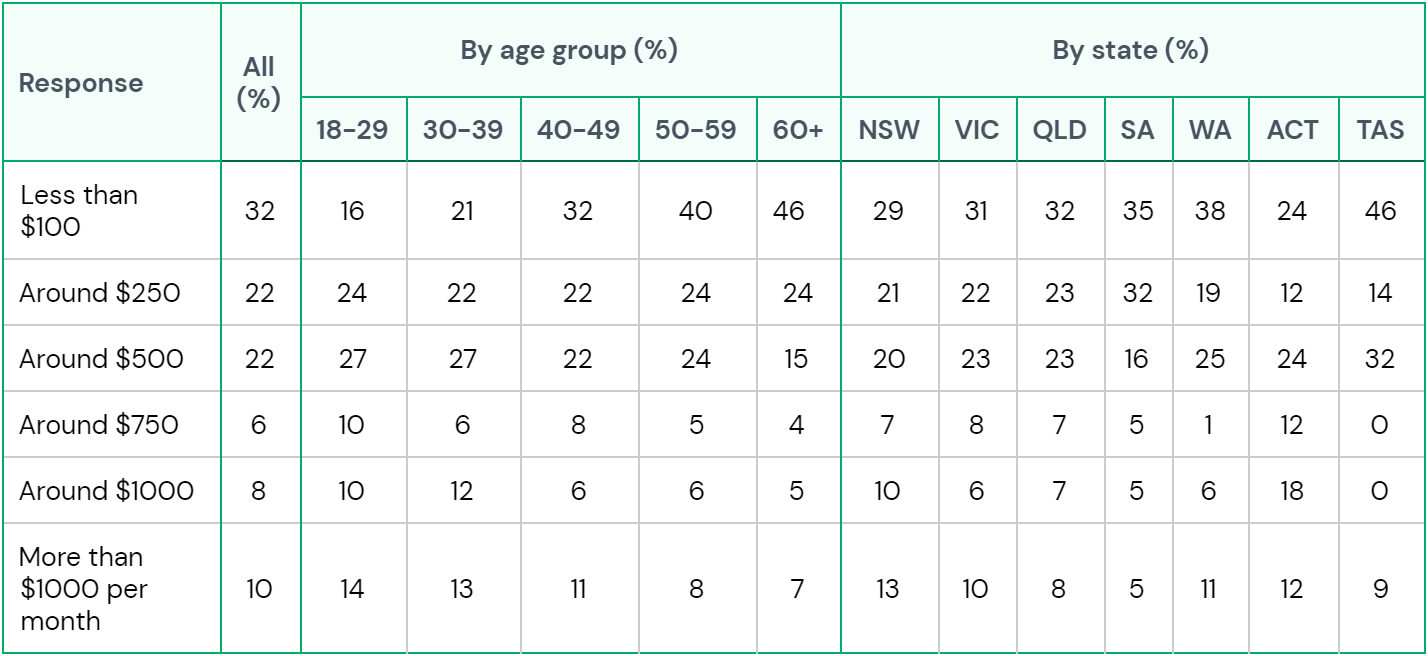

More importantly though, if you’re 30 you should 1) aim to have any high interest bad debt paid off at this point and 2) be trying to get your savings rate as high as possible. Obviously having a high salary is great, but what will be more impactful to growing your net worth is having a high savings rate. And in a survey done by money.com.au in 2020, they found that the average Australian is not doing a great job of saving at all, with over half of Aussies saving less than $250 a month.

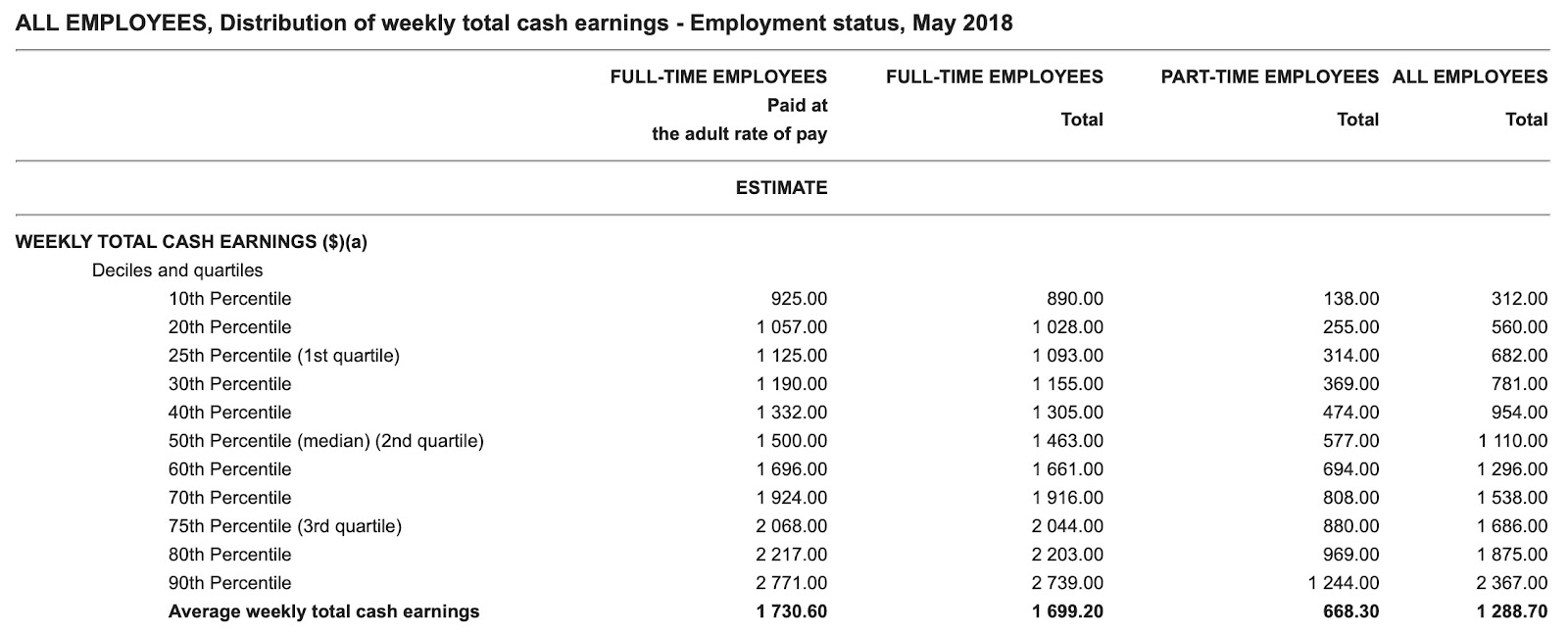

This might not seem too bad at first glance, but when you dig a bit deeper we find this is very low. If we look at ABS data in 2018 for median salary data we find the average Australian in earning $1110 a week, which comes out to $57K a year, and after tax that is $3800 in pocket a month. If they’re only saving $250 a month that’s a savings rate of 6%, far from ideal.

Now in this post we are mostly talking about averages but if you’re someone who is looking to retire as early as possible, an achievable benchmark (even on an average wage) is to save half your income, that’s a savings rate of 50%. If we look at saving 50% of an average wage $1900 a month vs the average of just $250 a month, after 20 years compounded at an average return of 8% a year, the difference would be $1,119,139 vs $147,255. A huge difference (of almost a million dollars over 20 years) that is really achievable by pretty much anyone that is willing to delay gratification in order to achieve financial independence.

This will require you to be regularly investing into the market and the best way for most people to do this is going to be via a broad market passive index ETF, which have historically returned 8-10% p.a over the long term. So make sure if you aren’t already that you begin getting into the habit of doing this.

Finally if you’re earning over $90K a year make sure to get private health cover by the time you are 31. Otherwise a 2% Lifetime Health Cover loading may be added to your private health cover premium for every year you haven’t held hospital cover, once you do take it out. This premium loading caps out at 70% but since you can get private hospital cover that is cheaper than the medicare levy surcharge, there is no reason you should ever be paying the medicare levy surcharge, or the loading premium.

40 years old

Average (Median) Net Worth At 40 Years Old: $97,425

Now moving onto 40 years old, reports from the Australian Bureau of Statistics (ABS) show that this is the time in your life when your income should be at its highest. You’ve had enough time to get experienced in your chosen profession and your wage will reflect this increased experience. This is why the average net worth at 40 has more than tripled since 30 and is $97,425.

And since your income is at its highest in your 40’s this is the time to really grow your net worth and the best way to do this is as I mentioned earlier, is by getting your savings rate as high as possible. Now most of the guides suggest having around 3X your salary in net worth at this point but I think if you’re reading this post, even with a conservative saving and investment strategy there is no reason you shouldn’t be able to have at least 5X, which would be around $300,000. Let me show you why, if you saved a modest $500 a month (13% of the after tax income of the average Australian wage), starting from literally $0, after 20 years of passive investing at 8% return you would have $294,510. And most of you will start with more than $0, and also be investing more than just 13% of your after tax salary, so while this looks like a lot, it’s definitely attainable.

Whilst it’s not for everybody if you are interested in real estate I would aim to have purchased a home by 40 as well. Since most mortgages are over 30 years, this will give you enough time to have it paid off. Whilst the percentage returns of real estate might not be better than stocks and even if the best years of real estate are behind us now, there are definitely still some very real reasons to consider getting into real estate. The main one being the ability to get extremely large amounts of leverage at really low interest rates, this is why even though the % returns might not be stocks, the dollar returns typically will be. There’s also a lot of tax advantages to owning a home and things that are harder to put a dollar value to, like not having to move around and having stability.

Now if you like your career and aren’t really interested in retiring early, this is a great time to start maxing your super contributions each year. Any amounts you contribute towards super (up to the cap of $25,000 a year) are only taxed at 15%, so for those of you with high marginal tax rates, this can be a significant risk free saving each year, that is really a no brainer if you don’t plan on retiring before the superannuation preservation age (this is the age if which you can access your super funds).

Regardless, probably the most important thing to do once you hit 40 is to start evaluating now whether you’re on track to hit your retirement goals (whatever they are), and you can do this by looking at what your average annual spend is. For example if you spend $40K a year, assuming a safe withdrawal rate of 4% a year, then you will need $1M saved to last you indefinitely, or if you’re more frugal and spend only $20K a year you’ll only need $500K saved in retirement. You can calculate this easily by just multiplying your expenses by 25.

50 years old

Average (Median) Net Worth At 50 Years Old: $194,850

Now if you’re 50 years old the average net worth is $194,850 and this is when compound interest generally takes over contributing more towards your net worth than your savings rate. For example if you have $200K invested with an 8% return, in 1 year that will grow by $16K and most people aren’t saving or investing more than $16K in a single year.

This is when you want to be maxing super contributions for sure, it’s a risk free profit and an absolute no brainer to start doing this at 50 since you’re so close to being able to access your super. And since you are close to that retirement age, you should also start thinking about moving your investment and super allocations into more defensive assets, like bonds and cash.

This is also when you want to make sure you don’t have any outstanding bad debt and you’re well on your way to having any good debt (like mortgages) paid off.

Now if you’re not on track to hit your retirement targets, this is the time to start considering ways to lower living expenses, cut down on spending, or moving to a lower cost of living area. Ideally you want to be in a position in your 50’s where if push comes to shove you’re able to leave your job and not be stressed about it at all.

60 years old

Average (Median) Net Worth At 60 Years Old: $290,975

At 60 years old the average net worth for Australian’s is $290,975 and the strategy and recommendations are exactly the same as at 50. Max super contributions, pay down all debt, move investments to more conservative options, and evaluate whether you are ready to retire. Which like I mentioned earlier all you need to do is take your average annual spending, multiply it by 25, and that is how much you need invested to live off the return indefinitely.

Summary and next steps

How to improve your net worth

Now the most important thing is not to stress too much if you’re not hitting these averages and goals, everyone’s situation is different and so are their retirement goals. And net worth certainly isn’t the most important thing in the world, what’s going to be more effective is learning to live and be happy with less money, as you most likely don’t need to be spending as much as you do!

Then from there as long as you start taking action early, with budgeting, taking advantage of compounding through investing and living below your means. If you can stay focused with this, for actually not too long of a time in the grand scheme of things (15 – 20 years), you can easily be retired before 45 even on an average wage. This is definitely not out of reach for anyone and it doesn’t require you to earn a massive salary or to follow some gurus advice on how you can easily make thousands of dollars passively by buying their ebook. Take steps to start investing for the long term using something like Index Funds and ETFs. Check out my step by step guide to investing in ETFs here.

Calculate when you can retire

Calculate your retirement age

If you want to get an idea of when you might be able to retire and reach financial independence, check out the below calculator. You’ll be able to answer the question: “At what age can I retire given my present retirement fund and future, planned investments?” The calculator creates an investment schedule and charts.

Retirement Age Calculator

Data used:

- https://www.fool.com.au/2019/10/23/how-wealthy-should-you-be-at-your-age-2/

- https://starinvesting.com.au/what-should-be-your-net-worth-right-now/

- https://mccrindle.com.au/insights/blog/australias-household-income-wealth-distribution/

- https://www.abs.gov.au/ausstats/abs@.nsf/Lookup/by%20Subject/6523.0~2017-18~Main%20Features~Key%20Findings~1

- https://www.money.com.au/aussie-saving-behaviours#Savings-level

This was super helpful, thank you.

What do you recommend for someone who is 50 – should I start investing or just start maxing my super contributions?